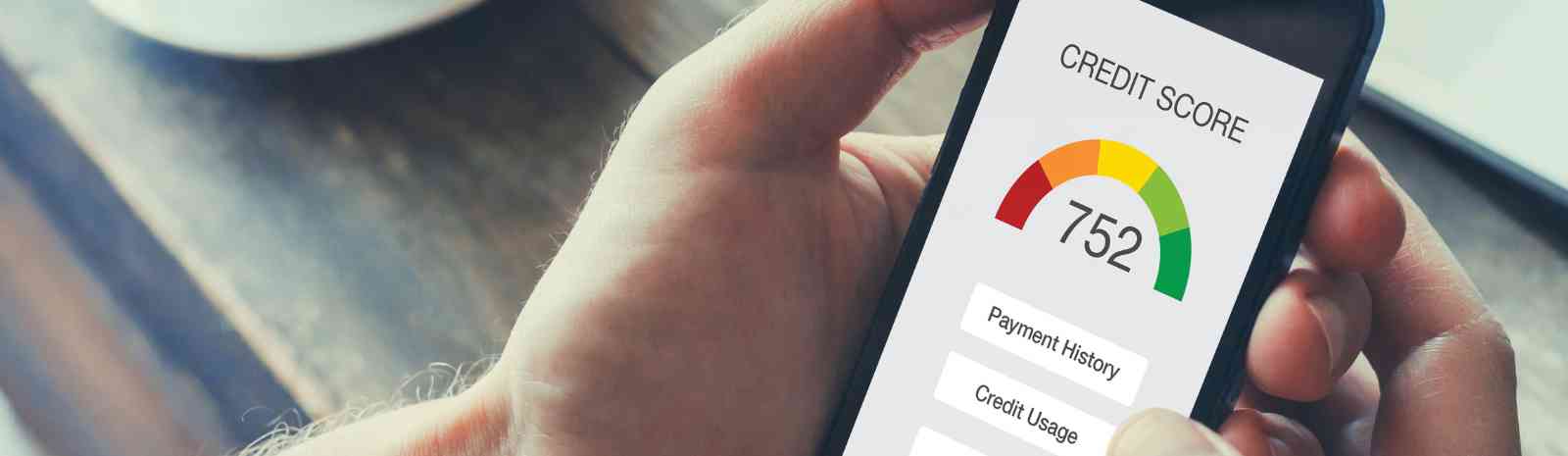

Improve your financial wellness with My Credit Manager. Understand, manage and protect your credit with this free tool located within The Dime Bank online and mobile banking.

Knowing your credit standing is essential when you want to apply for a loan or a credit card, but it’s also important to track changes to your score since it can alert you to suspicious activity. My Credit Manager gives you the tools to help protect your financial health.

With My Credit Manager you can:

- Stay on top of your credit with alerts if your score changes.

- See how your credit score might change when you take certain actions like applying for a loan or opening a new credit card.

- Track and manage your debt in one spot – easily see open balances and monthly payments and more.

There’s no cost to use My Credit Manager so log into your online and mobile banking and check your credit score today.

You’ll get 24/7 access to your credit report, a credit score simulator that can estimate your score before you open new lines of credit, and resources to learn more about managing your score.

We hope you take advantage of My Credit Manager to keep on top of your credit score.

My Credit Report faqs

- How do I dispute and correct inaccurate information in my credit report?

- How is my credit score calculated?

- How do I improve my credit score?

- Why is your score different from others I see?

- Why do the reported dates differ between accounts?

- How secure is my credit data?

- How frequently is my overall credit score updated?

- Can I get my credit information sent to my email?

- Will outstanding balances to the IRS show up on my credit?

- Can spouses access each other's information on shared accounts?

- How long do public records stay on my file?

- Can you provide me with a full background check so I can see more details?

- Can I dispute an Inquiry for a loan I never actually got?

- When will closed accounts come off my credit report?

- How do I lower the monthly payments on my loans?

If you discover information on your credit report that you believe is inaccurate, you can take the following steps to dispute and hopefully correct the information.

- Highlight the errors on your credit report.

- Gather supporting documents that show your side of the story; for example, receipts or bank records showing that you made a payment on time that’s recorded as late or delinquent.

- Submit the information to the bureaus with a brief explanation (100 words or less).

You may find that some companies have forms on their websites that you can use.

You can also submit your information directly to the reporting lender.

After you submit your claim, you may need to wait 30 to 45 days before it’s resolved, and the corrected information appears on your credit report. Note however, that if the inquiry confirms that the information is accurate, the bureau or lender won’t change it.

If you still have questions after your claim is rejected and want to pursue your dispute further, you can file a complaint against a bureau or lender with the Consumer Financial Protection Bureau or with the Attorney General of your state.

How is my credit score calculated?

In addition to calculating credit scores themselves, the three major credit bureaus, Equifax, Experian, and TransUnion, provide detailed information about a consumer’s credit activity to other companies that calculate a credit score. The two major companies providing credit scores are FICO® and VantageScore. Each uses a proprietary method to calculate their score. The exact mix may vary depending on company and type of loan.

In addition to calculating credit scores themselves, the three major credit bureaus, Equifax, Experian, and TransUnion, provide detailed information about a consumer’s credit activity to other companies that calculate a credit score. The two major companies providing credit scores are FICO® and VantageScore. Each uses a proprietary method to calculate their score. The exact mix may vary depending on company and type of loan.

Some of the items considered:

Payment history: Do you make your payments on time?

Amounts owed: Do you owe too much to too many lenders?

Length of credit history: Does your record show that you can maintain your commitment over a period of time?

New credit: Have you opened multiple new accounts in a short period of time?

Credit mix: Do you have a variety of account types, such as credit cards, installment loans, or a mortgage?

Utilization: The ratio between available credit and used credit.

Balance: Total amount of reported debt.

Available credit: Amount of credit available.

FICO Score categories

300 – 499: Very poor

500 – 600: Poor

601 – 660: Fair

661 – 780: Good

781 – 850: Excellent

300 – 499: Very poor

500 – 600: Poor

601 – 660: Fair

661 – 780: Good

781 – 850: Excellent

VantageScore categories

300 – 600: Subprime

601 – 660: Near prime

651 – 780: Prime

781 – 850: Superprime

FICO® produces several models of their FICO® Score to accommodate different types of lending. Models also vary depending on which bureaus provide the data for them. The most common model is FICO Score 8, which along with FICO Score 9 are widely used for lending. Both use data from all bureaus, as do most other models.

FICO® Score models that are more specific include FICO® Auto Score and FICO® Bankcard Score, for lending associated with car purchases and credit card applications. Scores for these models range from 250 – 900.

Mortgage lending uses FICO® Score 2, FICO® Score 5, and FICO® Score 4, which use data from only one of the three bureaus.

Disclaimer: FICO® Scores are developed independently by Fair Isaac Corporation. Most, but not all, lenders use FICO® Scores to determine a consumer's credit worthiness. We're not affiliated with FICO® and have no influence on producing a FICO® Score.

How do I improve my credit score?

You can take several steps to improve your credit score but be aware that there are no quick fixes. You may be able to see your score tick up soon after you start trying to improve it. However, credit reports are updated month by month and it may take several months or even years before your credit score is where you want it to be.

You can take several steps to improve your credit score but be aware that there are no quick fixes. You may be able to see your score tick up soon after you start trying to improve it. However, credit reports are updated month by month and it may take several months or even years before your credit score is where you want it to be.

- Pay your bills on time. Late and delinquent payments make up much of what determines your credit score. You need to establish a good record of timely payments. Consider setting up autopay for your accounts.

- Reduce your credit utilization. Credit utilization is another important factor in calculating your credit score. Keeping low balances on revolving accounts, such as credit cards, will help improve your score. You can also reduce credit utilization by requesting an increase in your credit line - as long as you don’t use the increase in your limit to increase debt.

- Avoid or limit opening new accounts, especially multiple accounts within a short period. When you apply for credit, the prospective lender makes a hard credit inquiry, which is reported to the bureaus. Lenders may interpret making multiple credit applications as you are facing financial troubles and looking to increase debt as a way out.

- If you have no credit history, or a thin credit history, you can look into other ways to get yourself on record as making timely payments. One solution is a credit builder loan, where you make payments into an account over a set period of time (usually one or two years). These payments are reported to the bureaus, so you build a credit history. If you pay monthly rent and utilities, you can look into rent reporting options. With rent reporting, your landlord or property management company reports your monthly rent and utilities to the bureaus.

- Keep older accounts open. Length of credit history works for you. The longer you have an account open, the more stable you look to the bureaus.

- Consolidate your debts. Too many accounts may work against you. If possible, reduce the number of accounts, but be careful of affecting credit utilization. Don’t max out an account by consolidating it.

- Use credit monitoring. Improving your credit score is a project, a credit monitoring app is a critical tool for helping you manage your credit profile.

Why is your score different from others I see?

Each of the three credit bureaus (Equifax, Experian, and TransUnion) uses a different model to calculate a credit score and each gathers data independently.

Each of the three credit bureaus (Equifax, Experian, and TransUnion) uses a different model to calculate a credit score and each gathers data independently.

The credit bureaus pull your information from many different sources (such as lenders, collections, court records) at different times, there will always be discrepancies at any particular time between the reports from each credit bureau.

The financial institutions and companies that provide your credit score use different methods. Some rely on FICO® Score and some rely on VantageScore. Even between those two companies, there are credit scores based on reports from one bureau, two bureaus, or all three bureaus.

Why do the reported dates differ between accounts?

Lenders generally update their data on a monthly basis. However, the lenders may report data at various times during the month. The differences in reporting dates shouldn’t vary by more than 30 days. If you’re waiting for a specific update, such as corrected information from a dispute, remember that it can take up to 45 days for the updated information to appear on your credit report.

How secure is my credit data?

Your credit data is fully encrypted and secure. No one else has access to your information.

How frequently is my overall credit score updated?

Your credit score is updated completely every 30 to 45 days.

Your credit score is updated completely every 30 to 45 days.

Can I get my credit information sent to my email?

You can securely access your credit information online or have it sent to you in the mail. For security reasons, we won’t send your credit information by email.

Will outstanding balances to the IRS show up on my credit?

The IRS doesn’t report your tax debt to the credit bureaus. Your tax return information is protected by law, so the IRS can’t disclose it to third parties. However, if the IRS has filed a Notice of Federal Tax Lien, your debt to the IRS enters into public record. Even though the debt is public, the credit bureaus won’t include it in their credit reports. However, it may be possible for a lender to find the information if they look through public records. You can avoid a tax lien by entering into a repayment agreement with the IRS.

If my spouse and I share lines of credit, mortgages, or loans, will I be able to access their information?

You and your spouse can see the information from all shared accounts, but having some shared accounts doesn’t allow you or them access information about any non-shared financial accounts.

How long do public records stay on my file?

Derogatory information can stay on your record for 7 – 10 years. It’s always good to review your records to ensure that the information is accurate. If you find something that you feel is inaccurate, take steps to dispute and correct it.

Can you provide me with a full background check so I can see more details?

You can get a comprehensive background check from several online service providers. We don’t provide a full background check, only a credit report and credit score.

Can I dispute an Inquiry for a loan I never actually got?

You can dispute it, however as part of your application, you would have provided signed permission for the lender to make a hard credit inquiry. The inquiry goes in your credit report whether you’re approved for the loan or not. It’s not likely that your dispute will prove successful unless the lender made an inquiry without your permission.

You can dispute it, however as part of your application, you would have provided signed permission for the lender to make a hard credit inquiry. The inquiry goes in your credit report whether you’re approved for the loan or not. It’s not likely that your dispute will prove successful unless the lender made an inquiry without your permission.

When will closed accounts come off my credit report?

Any accounts that were in good standing when you closed them will remain in your record for 10 years. Any negative information will remain for seven years.

How do I lower the monthly payments on my loans?

You can lower your monthly loan payments in a few ways:

- If you’re paying on multiple credit cards, you can consolidate your debt into one card. The payment on a single card will likely be lower than the total of the payments made to several cards.

- You can negotiate with your creditors to ask for a lower interest rate or lower monthly payments by extending the loan term.

Debt Analysis FAQs

Do creditors always always look at gross income instead of net when calculating debt to income ratio?

Yes. Creditors always use gross income (before taxes) when calculating your debt to income ratio.

Why am I not seeing all of the credit data I would expect?

Newer accounts may not show up on your credit report because the creditor hasn’t started reporting it yet.

What do I do if some of this information is incorrect?

If you see information in your credit report that you think is incorrect, you can dispute it with the creditor or the bureaus. For more information, see the question "How do I dispute and correct inaccurate information in my credit report?" in the My Credit Report FAQs section.

Credit Score Factors FAQs

- How are credit scores actually calculated?

- Do different bureaus calculate scores differently?

- How long does it take before a late payment stops impacting my score?

- What’s a charge off?

- What about debt collectors and my report?

- How long collections of public records stay on your credit report?

- Why don’t closed credit cards count toward credit age?

- Why do closed accounts count toward total accounts but not towards credit age?

- How many total accounts is too many accounts?

- Does it hurt if my accounts have a high balance or missed payments?

I see what high, medium, and low impact is but how are credit scores actually calculated?

There are several factors that contribute to calculating a credit score. In general, the bureau or company considers the following factors when calculating your credit score:

There are several factors that contribute to calculating a credit score. In general, the bureau or company considers the following factors when calculating your credit score:

- The number of accounts you have

- The types of accounts

- Your used credit vs. your available credit

- The length of your credit history

- Your payment history

These factors may be weighted differently by each bureau or company so credit scores may vary.

For more information, see the question "How is my credit score calculated?" in the My Credit Report FAQs section.

Do different bureaus calculate scores differently?

Yes, each of the three major credit bureaus - Equifax, Experian, and TransUnion - calculate credit scores differently. They also differ from other companies that calculate credit scores, such as FICO® and VantageScore.

Yes, each of the three major credit bureaus - Equifax, Experian, and TransUnion - calculate credit scores differently. They also differ from other companies that calculate credit scores, such as FICO® and VantageScore.

Each bureau or company weighs the various factors that go into their calculation differently. Also, lenders who report credit data may not report to all three bureaus, which will affect the calculation.

For more information, see the question "How is my credit score calculated?" in the My Credit Report FAQs section.

How long does it take before a late payment stops impacting my score?

Late payments will stay in your record for seven years. You can dispute a late payment report that you believe is in error, however you will need to provide proof, such as documentation that you did make the payment in question on time. If the information is accurate, however, you'll have to wait the full seven years before it clears.

What’s a charge off?

A charge off is an entry in your credit report that indicates that a creditor has tried and failed to get a debtor to make good on overdue payments and has closed their account. Once the creditor charges off an account, they will sell it to a debt collector who will pursue the debt further.

A charge off can have a strongly negative impact on your credit score.

If I’m contacted by a debt collector and I pay immediately, will the debt show up on my credit report anyway? Do I have a grace period?

If you’re contacted by a debt collector, it’s likely that your account is in default by more than 90 days, maybe as long as six months. The negative effect of having your account in collection is less than the effect that you will have already incurred from being late, 30 days overdue, 60 days overdue, and 90 days overdue. The negative effects of a payment that is successively overdue stack up and will stay on your credit report for seven years. Also, the information that the account was charged off (closed by the lender) will remain for the same amount of time regardless of whether you paid off the debt with the debt collector.

You may be able to work out a grace period with the lender before they send the debt to collection. However, once the debt is sold to the debt collector, the damage to your credit is already done.

What influences how long collections of public records stay on your credit report? Are there set periods of time per type of record?

A chapter 7 bankruptcy will remain on your credit report for 10 years. However, other negative information, including chapter 13 bankruptcy, will stay on your credit report for seven years. Accounts that you closed in good standing will remain in your record for 10 years. Accounts that were closed involuntarily will remain in your record for seven years.

The amount of time that bureaus keep this account information is driven by what the bureau’s customers want. Because financial institutions want this information when they determine risk in extending credit, the bureaus provide it. If financial institutions wanted the time period to be more or less than what it is now, the bureaus would change what they report.

Why don’t closed credit cards count toward credit age?

Credit age is the age of your open, active accounts. When you close an account, it’s no longer active and ceases to count towards credit age. Closed accounts will, however, continue to count towards payment history for up to 10 years for accounts closed in good standing and up to seven years for accounts that were closed involuntarily.

Why do closed accounts count toward total accounts but not towards credit age?

Closed accounts will continue to count towards payment history, but not towards total accounts or credit age. Closed accounts remain on your record for up to 10 years if you closed them in good standing. If an account was closed involuntarily, it will remain on your record for up to seven years.

Closing an account, however, may adversely affect your credit utilization ratio, which takes into account the amount of available credit compared to the amount of credit you’ve used. For example, if you have three credit cards with credit limits of $1000 each and a balance of $200 on one, $400 on another, and $0 on the third, you have a total credit limit of $3,000 of which $600 of credit is used. Your credit utilization ratio is 20%, which is pretty good. If you close the account that has a zero balance, you now have two accounts with a $2000 credit limit, of which $600 is used. Your new credit utilization ratio is 33%, which may negatively affect your credit score because, even though you haven’t added any debt, you now have a higher amount of debt in relation to your credit limit. Alternatively, if you paid off the credit card with a $400 balance and closed the account, you’d have a $2,000 limit, of which $200 is used. Your credit utilization ratio would then be 10%, which may improve your credit score.

Credit Score Simulator FAQs

How are the simulated scores calculated?

Credit Score Simulator uses calculations that are similar to Experian, which uses the VantageScore model.

Credit Score Simulator uses calculations that are similar to Experian, which uses the VantageScore model.

How accurate are these simulations?

Credit Score Simulator is an educational tool that you can use for estimating the effect of certain financial actions on your credit score - but remember, they’re estimations only, not predictions. Actual results may be different.

Credit Score Simulator is an educational tool that you can use for estimating the effect of certain financial actions on your credit score - but remember, they’re estimations only, not predictions. Actual results may be different.

Why is the maximum three months for what happens if I miss a payment on an account?

Timely payment on your accounts is important for your credit health. A payment is considered late if it’s made past the grace period (typically about 4 – 5 days) and before 30 days past due. At 30 days past due, which is a full payment cycle, your account will be considered in default. You’ll owe two monthly payments and incur the risk of damaging your credit. It gets worse at 60 days past due (when you now owe three monthly payments). At 90 days past due, your account will be considered delinquent.

The Dime Bank offers My Credit Manager as a tool to manage your credit and is not an offer to lend. The credit score in the tool is not used for loan rate, loan approval purposes, or to make loan decisions at The Dime Bank.

Open an Account

Better Banking.

In Person & Online.

We offer innovative online and mobile banking services to make managing your money easy along with the personal attention of employees who care about you.